Are you an entrepreneur or a business owner in search of funding options? Have you heard of venture debt? It’s a form of financing that may make sense for your growing business. Let’s explore what venture debt is, when it makes sense, and when it may not be the best option.

Venture debt is a hybrid financing option that combines elements of debt and equity financing. It can help companies obtain additional funding without diluting ownership or giving up control. However, like any financial decision, venture debt should be carefully considered and evaluated to determine if it’s the best fit for your business needs. Let’s dive in and learn more about when venture debt may make sense.

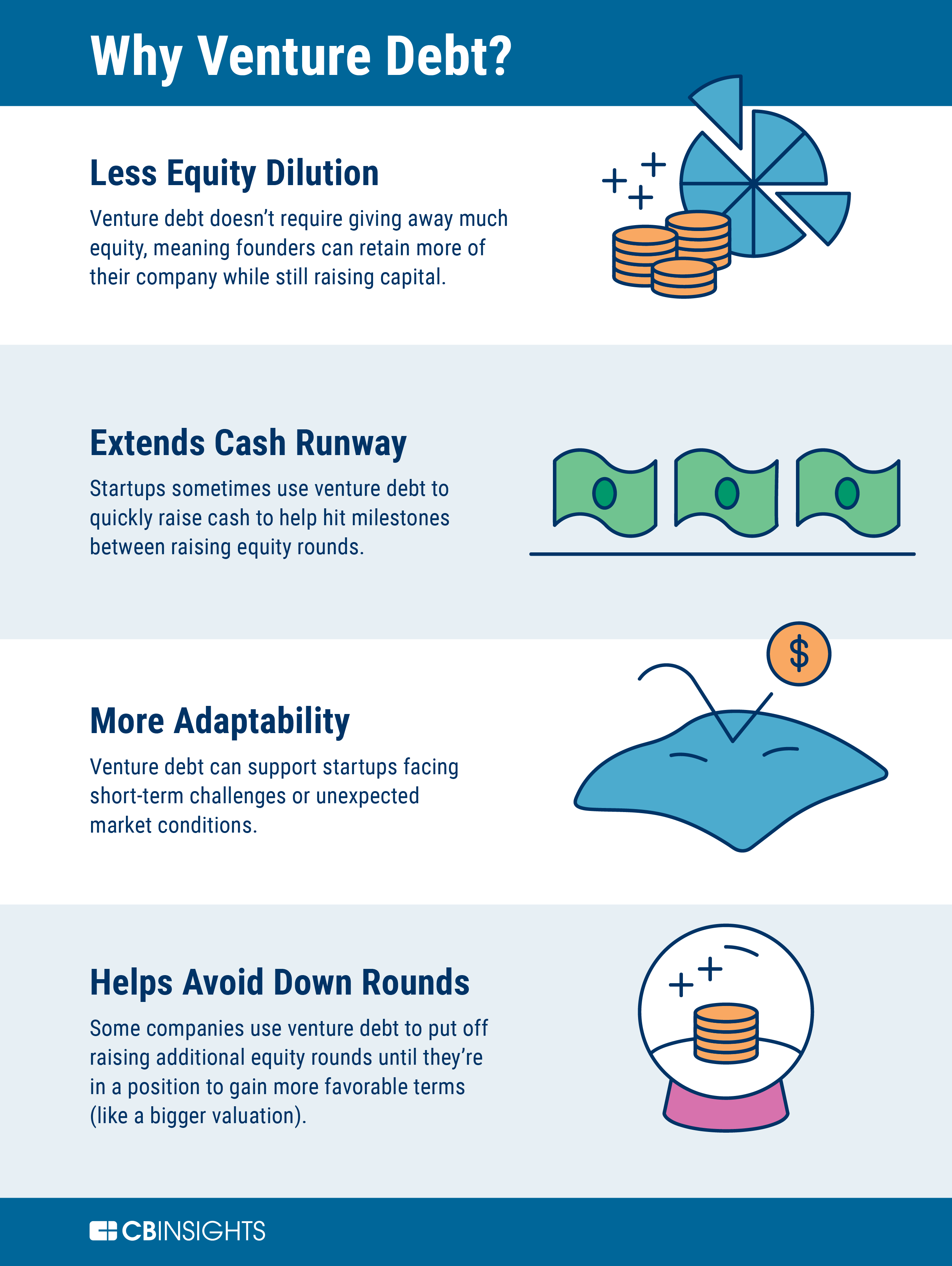

When Does Venture Debt Make Sense?

Venture debt is a form of financing that can be particularly attractive to startups and growing businesses. Unlike traditional equity financing, venture debt allows businesses to borrow funds without giving up any ownership or control of the company. However, venture debt isn’t right for every business. In this article, we’ll explore the circumstances when venture debt makes sense and when it doesn’t.

What is Venture Debt?

Venture debt is a form of debt financing that is typically offered to high-growth businesses that have already raised equity financing. This type of financing is often provided by specialized lenders who understand the unique needs of startups and growing businesses. Venture debt can be used to finance a variety of business needs, including expansion, working capital, and capital expenditures.

In exchange for the loan, the lender typically receives interest payments and may also receive warrants or options to purchase equity in the company. Unlike equity financing, venture debt does not dilute the ownership of existing shareholders.

When Does Venture Debt Make Sense?

1. Cash Flow Management

One of the main advantages of venture debt is that it can help businesses manage their cash flow. Unlike equity financing, where the funds are typically received in a lump sum, venture debt allows businesses to borrow funds as needed. This can be particularly useful for businesses that have uneven cash flows or seasonal revenue fluctuations.

2. Growth Capital

Venture debt can also be a good option for businesses that are in a growth phase. By borrowing funds, businesses can invest in marketing, product development, and other growth initiatives without diluting the ownership of existing shareholders.

3. Bridge Financing

Another use of venture debt is bridge financing. This type of financing is used to bridge the gap between equity rounds or other types of financing. Bridge financing can be particularly useful for businesses that need to finance short-term needs, such as inventory or payroll, while waiting for longer-term financing to come through.

4. Capital Expenditures

Venture debt can also be used to finance capital expenditures, such as equipment or real estate purchases. This can be particularly useful for businesses that need to make large purchases but don’t want to dilute the ownership of existing shareholders.

5. Lower Cost of Capital

Compared to equity financing, venture debt can be a lower cost of capital for businesses. This is because the interest rates on venture debt are typically lower than the cost of equity financing. This can be particularly useful for businesses that are looking to minimize their cost of capital.

When Doesn’t Venture Debt Make Sense?

1. Early-Stage Businesses

Venture debt is typically not suitable for early-stage businesses that have not yet raised equity financing. This is because these businesses may not have the cash flow or revenue to support debt payments.

2. Businesses with Unstable Cash Flows

Venture debt may not be suitable for businesses with unstable cash flows or revenue fluctuations. This is because the debt payments may be difficult to meet during lean times.

3. Businesses with Limited Growth Potential

Venture debt may not be suitable for businesses with limited growth potential. This is because the debt payments may become a burden if the business is not able to grow and generate sufficient cash flows.

4. Businesses with High Leverage

Venture debt may not be suitable for businesses that are already highly leveraged. This is because adding additional debt can increase the risk of default and bankruptcy.

5. Businesses with Limited Collateral

Finally, venture debt may not be suitable for businesses with limited collateral. This is because lenders may require collateral to secure the loan, and businesses without sufficient collateral may not be able to obtain financing.

Benefits of Venture Debt

There are several benefits of venture debt that make it an attractive financing option for startups and growing businesses. These include:

- No dilution of ownership

- Lower cost of capital compared to equity financing

- Flexible repayment terms

- Can be used for a variety of business needs

- Can help businesses manage cash flow

Venture Debt vs. Equity Financing

Venture debt and equity financing are two different ways of raising capital for a business. The main differences between the two are:

| Venture Debt | Equity Financing |

|---|---|

| No dilution of ownership | Dilutes ownership |

| Lower cost of capital | Higher cost of capital |

| Fixed repayment terms | No repayment terms |

| Can be used for a variety of business needs | Typically used for growth initiatives |

| Interest payments are tax deductible | Dividend payments are not tax deductible |

Conclusion

Venture debt can be a useful financing option for startups and growing businesses. It can help businesses manage their cash flow, finance growth initiatives, and provide lower cost of capital compared to equity financing. However, venture debt is not suitable for every business, and businesses should carefully consider their needs and financial situation before deciding whether to pursue venture debt.

Frequently Asked Questions

What is venture debt?

Venture debt is a type of debt financing that is typically provided to startup companies that have high growth potential but are not yet profitable. Unlike traditional bank loans, venture debt is usually structured as a term loan with a fixed interest rate and no equity component. It is often used in conjunction with equity financing to provide additional capital to support growth.

Venture debt can be a good option for startups that need to raise capital but don’t want to dilute their equity by issuing more shares. It can also be a good option for companies that are not yet profitable but have a clear path to profitability and need additional capital to get there.

How does venture debt differ from traditional bank loans?

Venture debt differs from traditional bank loans in several ways. First, venture debt is typically provided to startups that have high growth potential but are not yet profitable, whereas traditional bank loans are usually only provided to companies that have a proven track record of profitability.

Second, venture debt is often structured as a term loan with a fixed interest rate and no equity component, whereas traditional bank loans may have variable interest rates and may require collateral or a personal guarantee.

Finally, venture debt is often provided by specialized lenders who have experience working with startups, whereas traditional bank loans may be provided by larger, more established financial institutions.

What are the advantages of using venture debt?

There are several advantages to using venture debt. First, it can provide additional capital to support growth without diluting the company’s equity. This can be especially important for startups that are still in the early stages of growth and don’t want to give up too much ownership too quickly.

Second, venture debt can be less expensive than equity financing, as the interest rates are often lower than the cost of issuing new shares.

Finally, venture debt can help startups build relationships with specialized lenders who may be able to provide additional financing in the future.

What are the risks of using venture debt?

While there are advantages to using venture debt, there are also risks that should be considered. First, venture debt is still debt, and must be repaid with interest. This means that if the company is not able to generate enough cash flow to cover the debt payments, it may face financial difficulties.

Second, venture debt may be more expensive than traditional bank loans, as the lenders are taking on more risk by providing financing to startups that are not yet profitable.

Finally, if the company is not able to meet its growth projections, it may not be able to secure additional financing in the future, which could limit its ability to continue growing.

When does it make sense to use venture debt?

Venture debt can make sense for startups that have a clear path to profitability and need additional capital to support growth. It can also be a good option for companies that want to raise capital without diluting their equity too quickly.

However, venture debt should be used carefully, and companies should ensure that they have a solid plan for repaying the debt and generating enough cash flow to cover the debt payments. Additionally, companies should work with specialized lenders who have experience working with startups, as these lenders can provide valuable guidance and support throughout the financing process.

How to think about venture debt

In conclusion, venture debt can be a valuable tool for startups looking to raise capital without diluting their equity. However, it is important to carefully weigh the pros and cons before deciding if it is the right option for your business.

Firstly, it is important to have a clear understanding of your company’s financial needs and growth trajectory. Venture debt can be a good fit for companies that are generating positive cash flows and have a clear path to profitability.

Secondly, it is important to work with a reputable lender who understands the unique needs of startups. Look for a lender who has experience working with early-stage companies and can provide flexible terms and support throughout the funding process.

Lastly, it is important to have a plan in place for managing the debt and ensuring timely repayment. While venture debt can be a valuable tool for growth, it also comes with risks and should be managed carefully to avoid unnecessary financial strain on your business.

In summary, venture debt can be a smart option for startups looking to raise capital while minimizing equity dilution. However, it is important to carefully consider your company’s financial needs, work with a reputable lender, and have a plan in place for managing the debt.