Startups are one of the most exciting business ventures out there. They offer the opportunity for innovation, disruption, and the chance to make a real impact. However, with great opportunity comes great financial risk. This is why many startups turn to venture debt as a financing option.

Venture debt is a unique form of financing that allows startups to access capital without having to give up equity or control. In this article, we will explore the role of venture debt in startup financing, how it differs from traditional debt and equity financing, and its benefits and drawbacks. So, buckle up and let’s dive into the world of venture debt.

Understanding the Role of Venture Debt in Startup Financing

Venture debt is a type of debt financing for startups that complements equity financing. It is often used as a way to extend the runway of a startup by providing additional capital to fund growth initiatives that may not be immediately revenue-generating. In this article, we will explore the role of venture debt in startup financing and how it can benefit startups.

What is Venture Debt?

Venture debt is a type of debt financing that is provided to startups that have already raised equity financing. It is typically offered by specialized lenders who understand the unique needs of startups and are willing to take on the additional risk that comes with lending to early-stage companies.

Venture debt is structured differently from traditional debt financing. It often includes warrants or equity options that give the lender the right to purchase equity in the startup at a future date. This allows the lender to participate in the potential upside of the startup in addition to receiving interest payments on the debt.

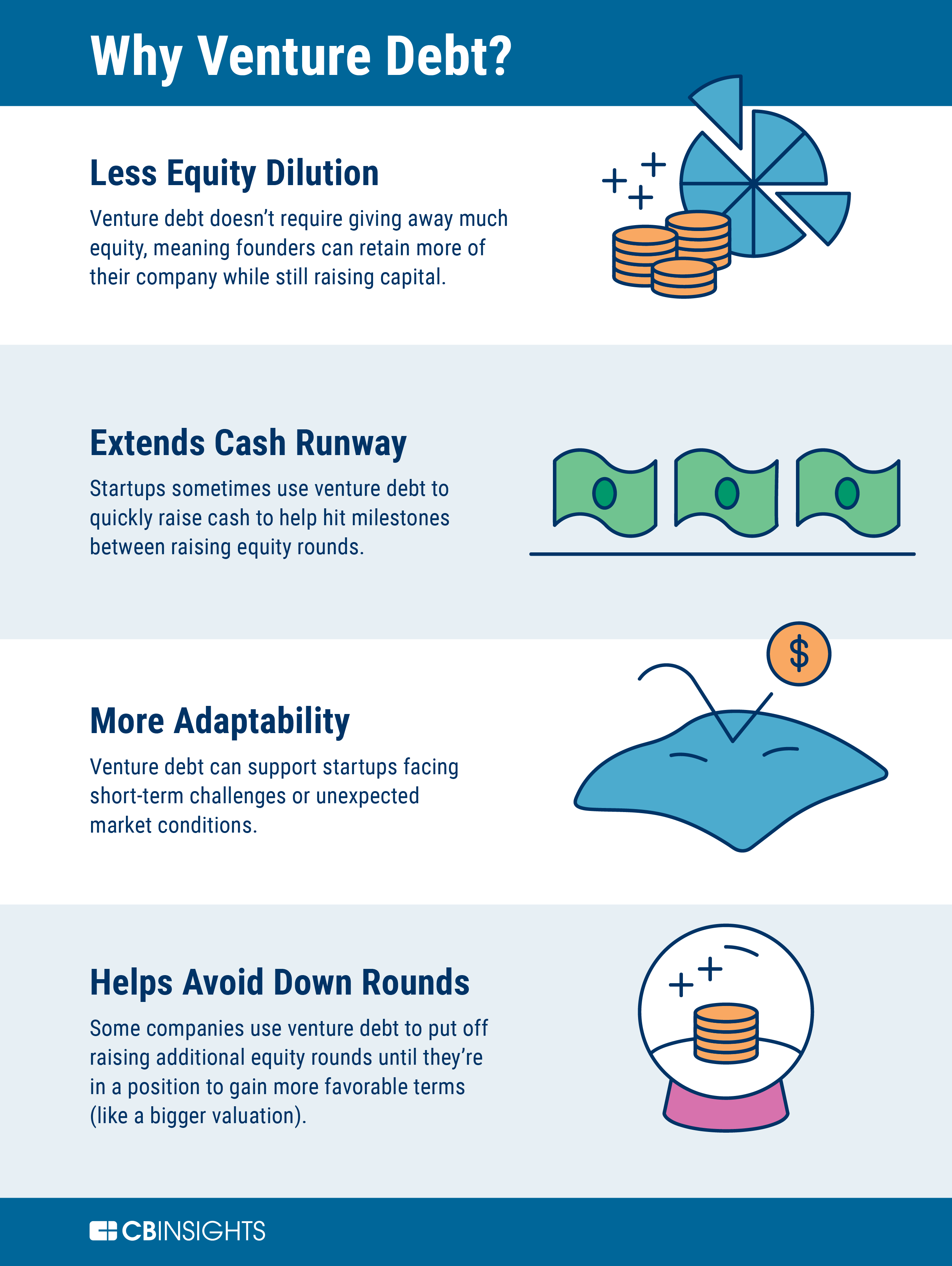

Benefits of Venture Debt

Venture debt can provide startups with several benefits, including:

- Extended Runway: Venture debt can provide startups with additional capital to extend their runway and fund growth initiatives. This can be especially useful for startups that may not be generating revenue yet but are still in a growth phase.

- Less Dilution: Because venture debt is structured differently from equity financing, it can be a way for startups to raise capital without diluting their ownership stake in the company.

- Flexible Terms: Venture debt can be structured in a way that is more flexible than traditional debt financing. This can include longer repayment terms, interest-only payments, and more.

Venture Debt vs. Traditional Debt Financing

Venture debt is often compared to traditional debt financing, but there are some key differences. Traditional debt financing typically requires collateral and may have more stringent repayment terms. Venture debt, on the other hand, is often unsecured and may have more flexible terms.

Venture debt is also often provided to startups that are not yet generating revenue, whereas traditional debt financing is typically only available to companies with a proven track record of revenue generation.

How is Venture Debt Structured?

Venture debt is often structured as a term loan or a line of credit. The terms of the loan will vary depending on the lender and the specific needs of the startup, but some common features of venture debt include:

- Interest Rates: Venture debt often comes with higher interest rates than traditional debt financing. This is because it is riskier for lenders to lend to startups that are not yet generating revenue.

- Warrants: As mentioned earlier, venture debt often includes warrants or equity options that give the lender the right to purchase equity in the startup at a future date.

- Covenants: Venture debt may include covenants that require the startup to meet certain financial metrics or other requirements. If the startup fails to meet these requirements, the lender may have the right to accelerate the repayment of the loan.

When is Venture Debt a Good Option?

Venture debt can be a good option for startups that have already raised equity financing and are looking for additional capital to fund growth initiatives. It can be especially useful for startups that are not yet generating revenue but are in a growth phase.

Venture debt may not be the best option for startups that are struggling to meet their existing debt obligations or for startups that are not yet at a stage where they can raise equity financing.

Conclusion

Venture debt can be a useful tool for startups that are looking for additional capital to fund growth initiatives. It can provide startups with a way to extend their runway and fund growth without diluting their ownership stake in the company. However, it is important for startups to carefully consider the terms of any venture debt financing and to ensure that it is a good fit for their specific needs and goals.

Frequently Asked Questions

1. How does venture debt differ from traditional bank loans?

Venture debt is a type of debt financing specifically designed for startups and high-growth companies. Unlike traditional bank loans, venture debt is typically provided by specialized lenders who understand the unique needs and risks of early-stage companies. In addition, venture debt often includes warrants or equity options, which can provide the lender with an opportunity to participate in the company’s future success.

While venture debt may have higher interest rates than traditional bank loans, it can be a valuable source of financing for companies that need to fund growth initiatives or bridge a financing gap between equity rounds.

2. What are the advantages of using venture debt in startup financing?

One of the main advantages of using venture debt is that it can help startups extend their cash runway without diluting equity. This can be especially valuable for companies that are not quite ready for another equity round, but need additional capital to fund growth initiatives. Venture debt can also provide startups with more flexibility than traditional equity financing, as there are fewer restrictions on how the funds can be used.

In addition, venture debt can be a good way for startups to build relationships with specialized lenders who may be able to provide additional funding in the future. Finally, because venture debt is typically structured to include warrants or equity options, lenders have an incentive to help the company succeed, which can lead to valuable strategic partnerships and introductions.

3. What are the risks associated with venture debt?

Like any form of debt financing, venture debt comes with risks that companies need to carefully consider. One risk is that the interest rates on venture debt can be higher than traditional bank loans, which can make it more expensive for the company to borrow money. Another risk is that venture debt is typically secured by the company’s assets, which means that if the company is unable to repay the debt, the lender may have the right to seize those assets.

In addition, because venture debt often includes warrants or equity options, the lender may have an incentive to push the company to take on more risk than it is comfortable with. Finally, if the company is unable to repay the debt, it may damage the company’s credit score and make it more difficult to secure financing in the future.

4. When is venture debt a good option for startups?

Venture debt can be a good option for startups that are looking to extend their cash runway without diluting equity. It can also be a good option for companies that are not quite ready for another equity round, but need additional capital to fund growth initiatives.

In addition, venture debt can be a good option for companies that have a clear path to profitability and are looking for financing to help them get there. Finally, because venture debt often includes warrants or equity options, it can be a good way for startups to build relationships with specialized lenders who may be able to provide additional funding in the future.

5. How can startups determine whether venture debt is the right financing option?

Startups should carefully consider their financing needs and goals before deciding whether venture debt is the right option for them. They should also weigh the risks and benefits of venture debt against other financing options, such as traditional bank loans or equity financing.

Finally, startups should do their due diligence on potential lenders, including understanding their track record, fees, and terms. By carefully evaluating their options and working with reputable lenders, startups can make an informed decision about whether venture debt is the right financing option for them.

Venture Debt VS Equity Financing for a high-growth startup?

In conclusion, venture debt has become an increasingly popular option for startups looking to secure financing. It offers a unique set of advantages, including lower equity dilution and increased flexibility in repayment terms. Venture debt can help startups bridge financing gaps and extend their runway, providing them with more time to grow and achieve profitability.

However, it’s important to keep in mind that venture debt is not a one-size-fits-all solution. Startups need to carefully consider their financing needs and goals before deciding whether venture debt is the right option for them. They also need to be aware of the potential risks and drawbacks associated with this type of financing, such as higher interest rates and stricter loan covenants.

Overall, venture debt can be a valuable tool for startups looking to raise capital and achieve their growth objectives. By exploring all of the available financing options and carefully evaluating their needs and goals, startups can make informed decisions about which type of funding is best suited for their unique circumstances.