Venture debt can be a useful tool for startups looking to fund their growth without diluting equity. However, it’s important to consider several factors before deciding if venture debt is the right option for your company. In this article, we’ll take a closer look at the key factors to consider before taking on venture debt, helping you make an informed decision for your business.

Understanding Venture Debt: Factors to Consider Before Getting It

Venture debt is a type of debt financing that is usually provided to startups and growing businesses that are not yet profitable. Unlike traditional bank loans, venture debt typically comes in the form of a loan that is secured by the company’s assets or equity. While venture debt can offer a number of benefits, it’s important to carefully consider the factors involved before deciding whether it’s the right financing option for your business. In this article, we’ll explore the factors you should consider before getting venture debt.

1. Your Company’s Stage of Development

One of the most important factors to consider before getting venture debt is your company’s stage of development. As mentioned earlier, venture debt is typically provided to startups and growing businesses that are not yet profitable. If your company is still in the early stages of development, it may not be the best fit for venture debt. In general, businesses that have already achieved some level of success and are generating revenue are better candidates for this type of financing.

When considering your company’s stage of development, it’s important to also take into account your growth plans. If you’re planning to rapidly expand your business, venture debt can be a good way to finance that growth. However, if you’re not planning to grow quickly, or if you don’t have a clear plan for growth, venture debt may not be the best option for your business.

2. Your Company’s Financial Situation

Another important factor to consider is your company’s financial situation. While venture debt can provide much-needed financing, it can also be risky if your business is not in a strong financial position. Before getting venture debt, it’s important to review your financial statements and projections to ensure that you have the cash flow to make the necessary payments.

If your business has a history of profitability, it may be easier to secure venture debt financing. However, if your business is not yet profitable, you may need to provide additional collateral or personal guarantees to secure the loan.

3. The Terms of the Loan

When considering venture debt, it’s important to carefully review the terms of the loan. This includes the interest rate, repayment schedule, and any additional fees or charges. You should also consider whether the loan requires any personal guarantees or collateral.

In general, venture debt tends to have higher interest rates than traditional bank loans. However, it may also offer more flexible repayment terms and fewer restrictions on how the funds can be used. It’s important to carefully consider the terms of the loan to ensure that they align with your business needs and financial goals.

4. The Size of the Loan

The size of the loan is another important factor to consider. While venture debt can provide much-needed financing, it’s important to ensure that you’re not taking on too much debt. Before getting venture debt, you should carefully consider how much financing you need and how much you can realistically afford to repay.

5. The Purpose of the Loan

It’s also important to consider the purpose of the loan. Venture debt can be used for a variety of purposes, including financing growth, expanding operations, or acquiring new assets. However, it’s important to ensure that the purpose of the loan aligns with your business goals and that you have a clear plan for how the funds will be used.

6. The Lender

When considering venture debt, it’s important to carefully evaluate the lender. This includes reviewing the lender’s reputation, track record, and experience working with businesses in your industry. You should also consider the lender’s requirements for collateral or personal guarantees, as well as their interest rates and repayment terms.

7. Your Business Plan

Before getting venture debt, it’s important to have a clear business plan in place. This should include your growth plans, financial projections, and a detailed plan for how you will use the funds from the loan. Having a strong business plan can help you secure more favorable loan terms and ensure that you’re using the funds in the most effective way possible.

8. Your Risk Tolerance

Venture debt can be a risky financing option, especially for startups and growing businesses. Before getting venture debt, it’s important to carefully evaluate your risk tolerance and determine whether you’re comfortable taking on this type of debt. You should also consider the potential impact of the loan on your business if you’re unable to make the necessary payments.

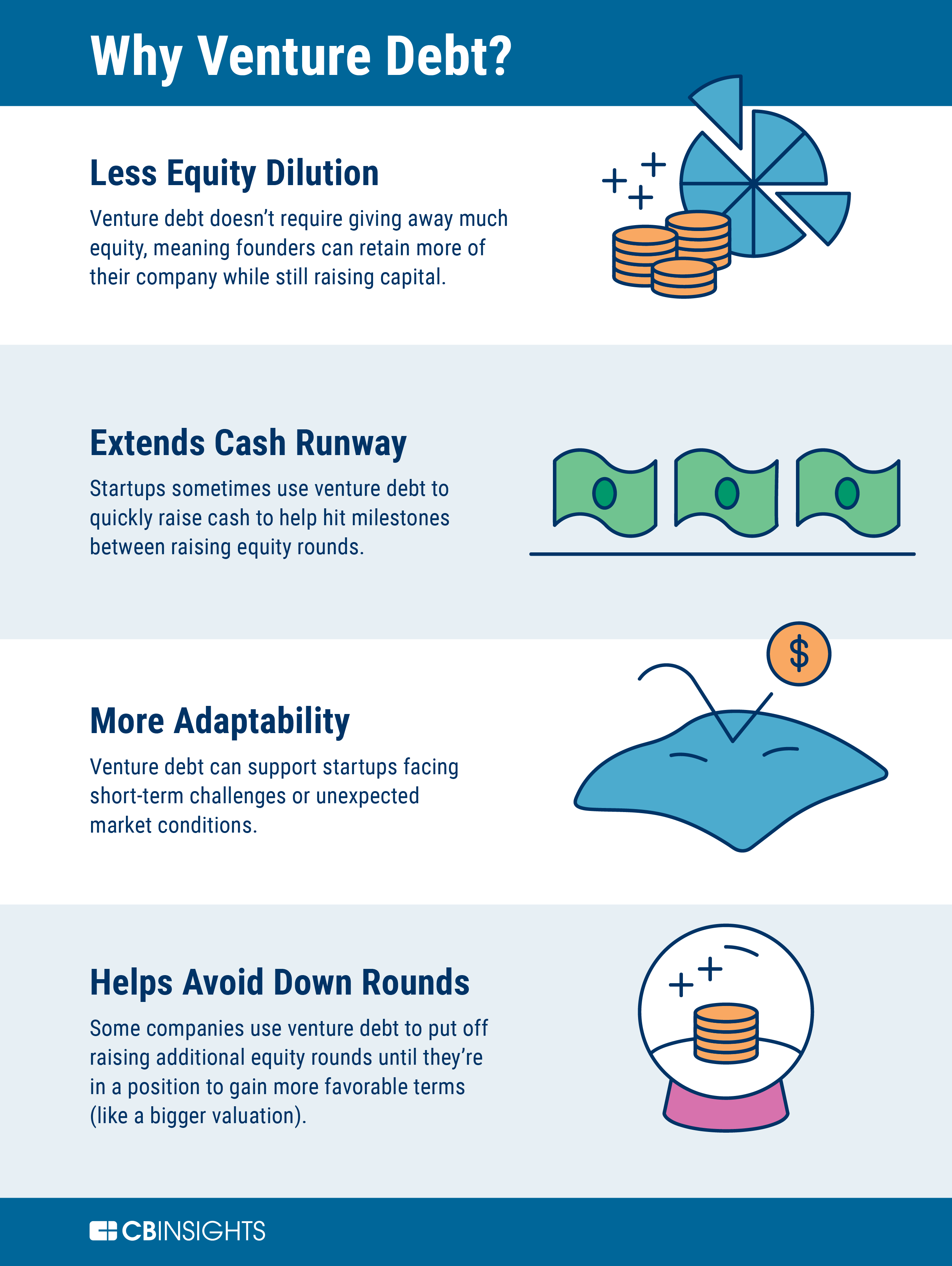

9. The Benefits of Venture Debt

While venture debt can be risky, it can also offer a number of benefits. For example, it can provide much-needed financing for growth and expansion, while allowing you to retain ownership and control of your business. It can also be a good way to build your business credit and establish relationships with lenders that can provide additional financing in the future.

10. Venture Debt vs. Other Financing Options

Finally, it’s important to consider how venture debt compares to other financing options, such as equity financing or traditional bank loans. While each financing option has its own benefits and drawbacks, venture debt can be a good option for businesses that want to retain ownership and control while still accessing much-needed financing. However, it’s important to carefully evaluate all of your options before making a decision.

In conclusion, venture debt can be a valuable financing option for startups and growing businesses that are not yet profitable. However, it’s important to carefully consider the factors involved before deciding whether it’s the right option for your business. By evaluating your business’s stage of development, financial situation, and growth plans, as well as the terms of the loan, lender, and purpose of the loan, you can make an informed decision about whether venture debt is the right choice for your business.

Frequently Asked Questions

What is venture debt?

Venture debt is a type of debt financing that is usually provided to startups and growing businesses that have raised equity capital. This type of debt is usually provided by specialized lenders who are familiar with the needs of startups and are willing to take on higher risk in return for higher interest rates.

Venture debt is typically used to finance growth initiatives such as expanding sales and marketing efforts, launching new products, or entering new markets. It can also be used to extend the runway of a startup while it is raising additional equity capital.

What are the advantages of venture debt?

There are several advantages of venture debt compared to equity financing. First, venture debt does not dilute the ownership of the company’s existing shareholders, which means that the founders and early investors can retain a larger percentage of the company’s equity.

Second, venture debt is usually less expensive than equity financing because the interest rates are lower than the expected return on equity investments. Finally, venture debt providers are not typically involved in the day-to-day operations of the company, which means that the management team can maintain control of the company’s strategic direction.

What are the factors to consider before getting venture debt?

Before getting venture debt, there are several factors that you should consider. First, you should assess whether your business is suitable for venture debt. Venture debt is typically only appropriate for businesses that have a proven track record of growth and profitability, or that are close to achieving profitability.

Second, you should consider the cost of venture debt. While venture debt is typically less expensive than equity financing, the interest rates are still higher than traditional bank loans. You should also consider the fees associated with venture debt, such as origination fees and closing costs.

What are the risks of venture debt?

Like any form of debt financing, venture debt carries risks for the borrower. The primary risk is that the borrower may not be able to make the required payments on the debt, which could result in default and the loss of assets. Additionally, because venture debt is typically secured by the company’s assets, the lender may have the right to seize those assets if the borrower defaults.

Another risk of venture debt is that it can limit the company’s flexibility. Because venture debt typically comes with covenants and other restrictions, the borrower may be limited in its ability to take on additional debt or to make other strategic decisions.

How do I find a venture debt provider?

Finding a venture debt provider can be challenging, as there are relatively few lenders in this space. One approach is to ask your existing investors for recommendations, as they may have relationships with venture debt providers. You can also search online for venture debt providers or attend industry conferences to network with potential lenders.

When evaluating venture debt providers, it is important to assess their experience working with startups, their reputation in the industry, and their terms and conditions. You should also carefully review the loan agreement and seek legal advice before signing any documents.

In conclusion, there are several factors to consider before getting venture debt. The first and foremost is to ensure that the business has a clear plan and strategy for growth. This means having a solid understanding of the market, competition, and customer needs. It is also important to have a strong management team in place with a track record of success.

Another important factor to consider is the financial health of the business. Lenders will want to see that the company has a history of generating revenue and is capable of repaying the loan. It is also important to have a realistic plan for how the loan will be used and how it will contribute to the company’s overall growth strategy.

Finally, it is important to consider the terms and conditions of the loan. This includes the interest rate, repayment schedule, and any fees associated with the loan. It is important to carefully review these terms and ensure that they align with the company’s financial goals and capabilities.

In summary, before getting venture debt, businesses should have a clear plan for growth, a strong management team, financial stability, and a thorough understanding of the terms and conditions of the loan. By considering these factors, businesses can make informed decisions about whether or not venture debt is the right financing option for their needs.