Venture debt and traditional bank loans are two popular financing options for businesses. While both provide access to capital, they differ in several key ways. Understanding the advantages and disadvantages of each can help entrepreneurs make informed decisions about their financial needs. In this article, we’ll explore the similarities and differences between venture debt and traditional bank loans, and help you determine which option might be right for your business.

Comparing Venture Debt and Traditional Bank Loans: Which is Better?

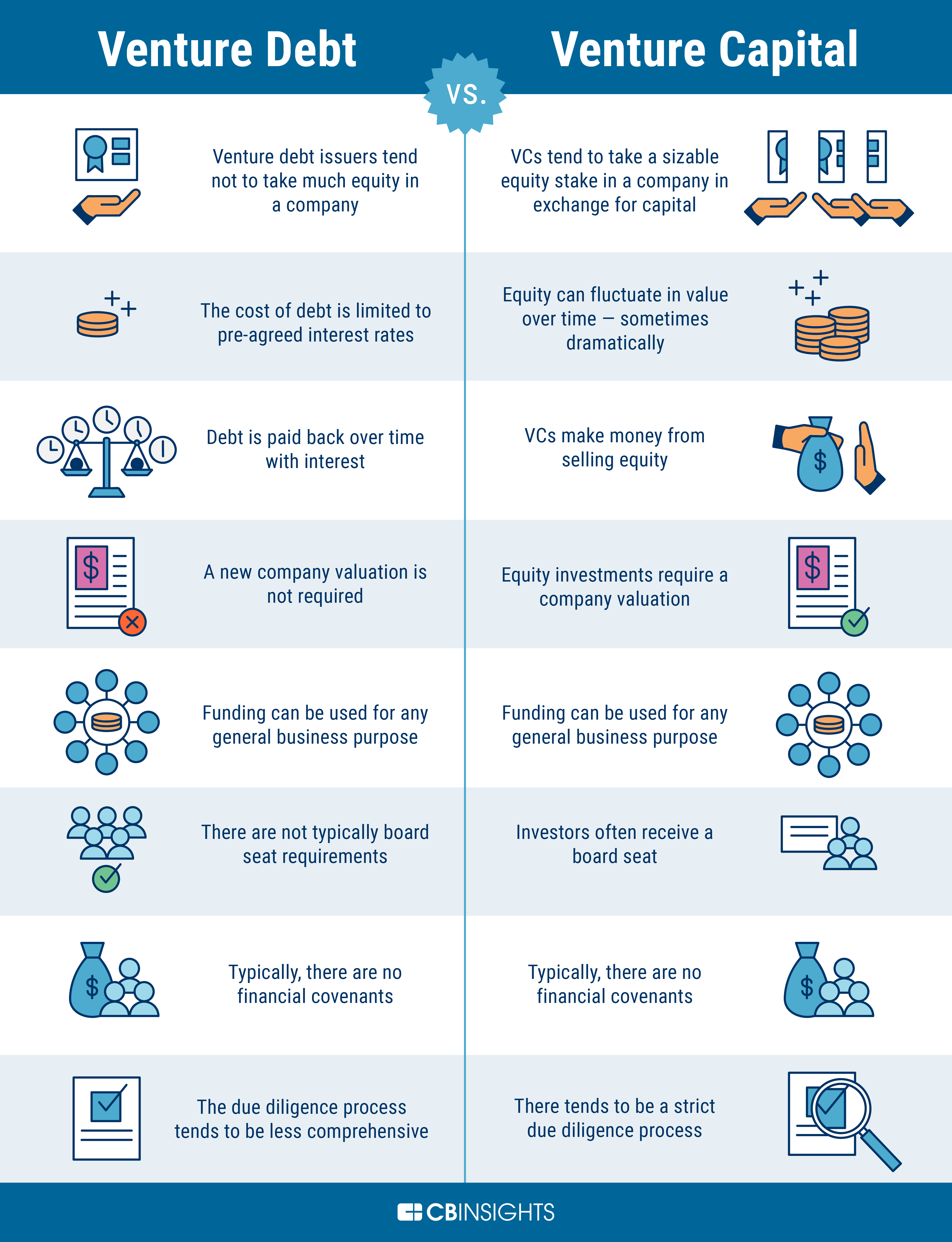

What is Venture Debt?

Venture debt is a type of debt financing that is typically provided to high-growth startups and emerging companies. Unlike traditional bank loans, venture debt is often provided by specialized lenders who understand the unique needs of these types of companies. Venture debt can be used to fund a variety of business needs, including working capital, capital expenditures, and even to fund acquisitions.

Venture debt is typically structured as a loan with a set interest rate and a repayment schedule, similar to a traditional bank loan. However, venture debt lenders may also receive warrants or equity in the company as part of the deal, which can provide additional upside potential for the lender.

What are Traditional Bank Loans?

Traditional bank loans are a type of debt financing that is provided by banks and other financial institutions. These loans are typically secured by collateral, such as real estate or equipment, and have a set interest rate and repayment schedule. Traditional bank loans are often used to fund long-term investments, such as the purchase of a new building or the acquisition of another company.

Unlike venture debt, traditional bank loans do not typically provide lenders with warrants or equity in the company. Instead, the lender receives interest payments and, in the event of default, may foreclose on the collateral.

Pros and Cons of Venture Debt

Pros:

- Flexible repayment terms

- Can be used to fund a variety of business needs

- May provide additional upside potential for the lender

Cons:

- Can be more expensive than traditional bank loans

- May involve giving up equity or warrants in the company

- May be more difficult to secure than traditional bank loans

Pros and Cons of Traditional Bank Loans

Pros:

- Typically lower interest rates than venture debt

- May be easier to secure than venture debt

- Collateral can help mitigate lender risk

Cons:

- Less flexible repayment terms than venture debt

- May not be suitable for all business needs

- Does not provide lenders with equity or warrants in the company

How do Venture Debt and Traditional Bank Loans Compare?

Interest Rates: Venture debt typically has higher interest rates than traditional bank loans, due to the increased risk associated with lending to high-growth startups. However, the interest rates on venture debt can be more flexible than traditional bank loans, and may be structured as a combination of fixed and variable rates.

Repayment Terms: Venture debt typically has more flexible repayment terms than traditional bank loans. These terms may be structured to align with the company’s growth and cash flow projections, which can help to make the debt more manageable. Traditional bank loans, on the other hand, typically have fixed repayment terms that may not be as flexible.

Risk: Venture debt is generally considered to be riskier than traditional bank loans, due to the fact that it is typically provided to high-growth startups that may not have an established track record. However, venture debt lenders may mitigate this risk by securing warrants or equity in the company as part of the deal.

Uses: Venture debt can be used to fund a variety of business needs, including working capital, capital expenditures, and acquisitions. Traditional bank loans, on the other hand, are typically used to fund long-term investments, such as the purchase of a new building or the acquisition of another company.

Conclusion: Which is Better?

There is no one-size-fits-all answer to the question of whether venture debt or traditional bank loans are better. It ultimately depends on the specific needs of the company and its growth trajectory.

Venture debt may be a good option for high-growth startups that need flexible financing to support their growth. However, it may be more expensive than traditional bank loans and may involve giving up equity or warrants in the company.

Traditional bank loans may be a good option for companies that have an established track record and need financing for long-term investments. However, they may be less flexible than venture debt and may not be suitable for all business needs.

In the end, the decision between venture debt and traditional bank loans will depend on a variety of factors, including the company’s growth trajectory, financing needs, and risk tolerance. It is important for companies to carefully consider their options and work with a trusted advisor to determine which financing option is best for their specific needs.

Frequently Asked Questions

What is venture debt?

Venture debt is a type of financing where a lender provides debt capital to startup companies that have already raised equity financing. This debt is usually secured by the company’s assets, including intellectual property, and may also include warrants or equity options. Venture debt is considered a higher-risk investment than traditional bank loans, but it can also offer higher returns.

Venture debt is typically used by startups that need additional capital to accelerate growth, fund acquisitions, or extend their runway. It is often used in conjunction with equity financing, as it allows startups to minimize dilution while still getting the funds they need to grow.

How does venture debt differ from traditional bank loans?

Venture debt differs from traditional bank loans in several ways. First, venture debt is generally offered by specialized lenders who understand the needs and risks of startup companies. These lenders are often more flexible than traditional banks, offering customized loan structures and more lenient underwriting criteria.

Second, venture debt is typically secured by the company’s assets, including intellectual property, rather than by collateral such as real estate or equipment. This can make it easier for startups with limited assets to qualify for financing. Finally, venture debt often includes equity options or warrants, which give the lender the right to purchase shares in the company at a later date. This can provide additional upside potential for the lender.

What are the advantages of venture debt?

Venture debt offers several advantages over traditional bank loans. First, it allows startups to raise additional capital without diluting their ownership or giving up control. This can be particularly attractive for founders who want to maintain a larger stake in their company.

Second, venture debt can be more flexible than traditional bank loans, with customized loan structures that can be tailored to the needs of the company. Finally, venture debt can offer higher returns than traditional bank loans, as it is considered a higher-risk investment.

What are the risks of venture debt?

Venture debt is considered a higher-risk investment than traditional bank loans. Startups that take on venture debt are often in the early stages of growth and may have limited operating history or revenue. This can make it difficult for lenders to assess the creditworthiness of the company and the likelihood of repayment.

In addition, venture debt is typically secured by the company’s assets, which can include intellectual property. If the company fails to repay the loan, the lender may have the right to seize these assets, which could have a negative impact on the company’s ability to continue operating.

When should a startup consider venture debt?

Startups should consider venture debt when they need additional capital to accelerate growth, fund acquisitions, or extend their runway, but don’t want to dilute their ownership or give up control. Venture debt can be a good option for startups that have already raised equity financing and are in a strong financial position, with a clear path to profitability.

Startups should also consider the risks of venture debt and weigh them against the potential benefits. It’s important to work with a lender who understands the needs and risks of startups and can provide customized loan structures that meet the company’s needs.

Venture Debt VS Equity Financing for a high-growth startup?

In conclusion, venture debt and traditional bank loans are two financing options available to entrepreneurs. While both options have their pros and cons, venture debt offers more flexibility and is a good option for companies with high growth potential. Traditional bank loans, on the other hand, are more suitable for established companies with a strong credit history.

When it comes to venture debt, it offers lower interest rates and does not require collateral, which can make it an attractive option for startups. Moreover, venture debt offers a higher level of flexibility, as it allows companies to borrow money without giving up equity.

On the other hand, traditional bank loans are more suited to established companies that have a good credit history and are looking for long-term financing. While traditional loans can be harder to obtain, they typically offer lower interest rates and longer repayment terms, making them a good option for companies looking to finance large projects or acquisitions.

Ultimately, the choice between venture debt and traditional bank loans will depend on the specific needs of your business. It is important to carefully consider your financing options and choose the one that best suits your company’s growth and financial goals.