Entrepreneurship is a risky business, and funding is one of the main challenges for most startups. While traditional funding options such as venture capital and bank loans are available, venture debt is an increasingly popular option for many businesses. However, there is a common concern among entrepreneurs about whether personal guarantees are required for venture debt.

The answer is not black and white, as it largely depends on the lender’s policies and the borrower’s financial standing. In this article, we will explore the topic of personal guarantees in venture debt and provide insights to help entrepreneurs make informed decisions.

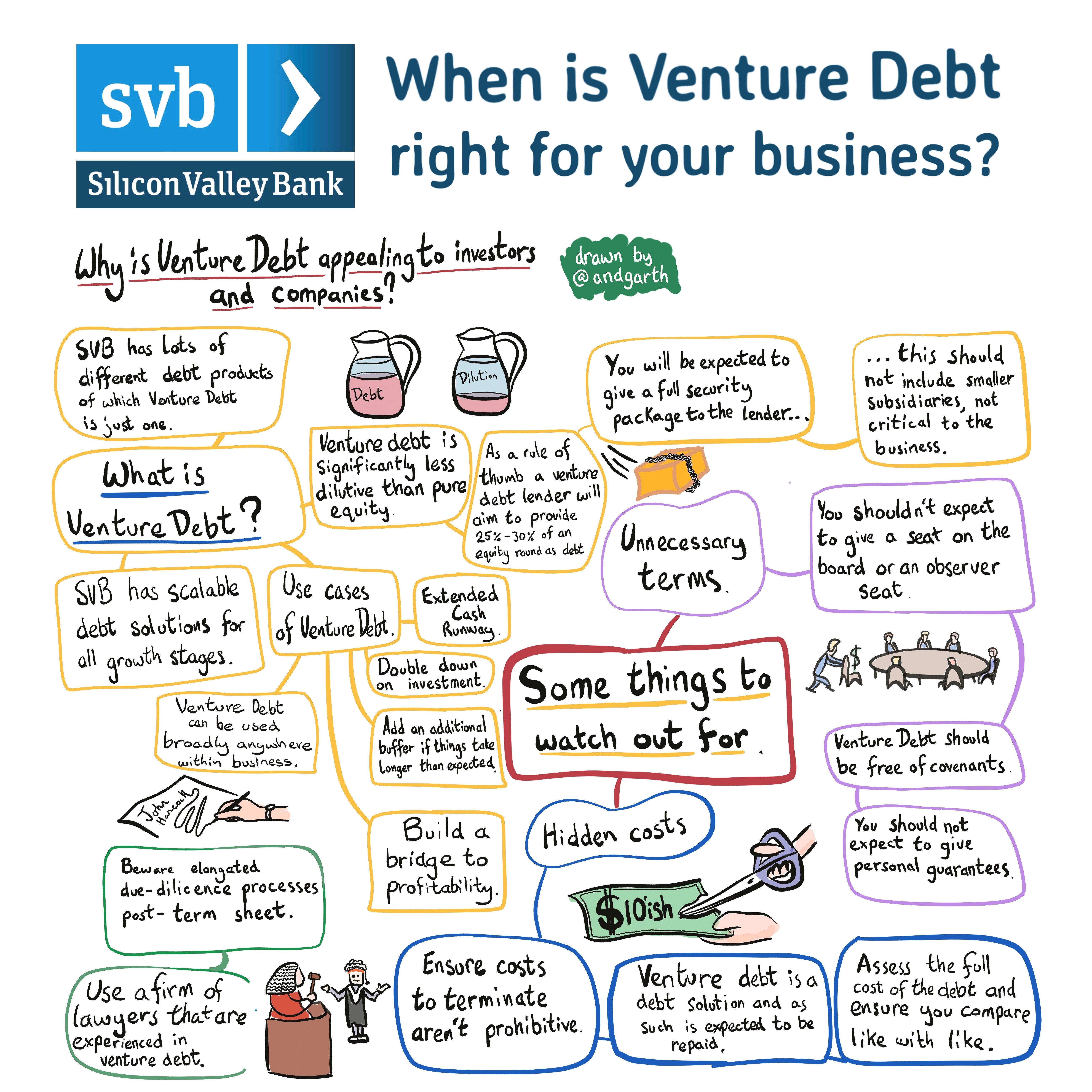

Does Venture Debt Require Personal Guarantees?

Venture debt is a type of financing that is commonly used by startups and growing companies to fund their operations. Unlike equity financing, venture debt does not require the company to issue shares of stock to investors. Instead, it involves borrowing money from a lender in exchange for a promise to repay the loan with interest.

What is Venture Debt?

Venture debt is a type of debt financing that is typically provided to early-stage companies that have a proven track record of growth. The funds are structured as a loan, and the borrower is required to make regular payments of principal and interest. Venture debt can be used for a variety of purposes, such as funding new product development, expanding into new markets, or acquiring other companies.

Benefits of Venture Debt

One of the key benefits of venture debt is that it allows companies to fund their growth without diluting their ownership. Unlike equity financing, venture debt does not require the company to issue shares of stock to investors. This can be particularly important for early-stage companies that want to retain as much ownership as possible.

Another benefit of venture debt is that it can be obtained relatively quickly and easily. Unlike traditional bank loans, which can require extensive documentation and collateral, venture debt lenders are typically more focused on the company’s growth potential and future cash flows.

Personal Guarantees in Venture Debt

While venture debt does not require the company to issue shares of stock to investors, it often does require some form of security or collateral. In many cases, this takes the form of a personal guarantee from the company’s founders or other key executives.

A personal guarantee is a legal agreement that makes the guarantor personally liable for the debt if the company cannot repay it. This means that if the company defaults on the loan, the guarantor’s personal assets may be seized to repay the debt.

When is a Personal Guarantee Required?

The requirement for a personal guarantee in venture debt financing depends on a variety of factors, including the size of the loan, the company’s creditworthiness, and the lender’s risk tolerance. In general, larger loans and riskier companies are more likely to require a personal guarantee.

Benefits of Personal Guarantees

While personal guarantees can be a burden for founders and other key executives, they can also provide some benefits. For example, a personal guarantee can help to demonstrate to lenders that the borrower is committed to repaying the debt. This can help to lower the interest rate or improve the loan terms.

Drawbacks of Personal Guarantees

On the other hand, personal guarantees can also be a significant risk for the guarantor. If the company defaults on the loan, the guarantor may be held personally liable for the entire amount of the debt. This can lead to financial ruin for the guarantor and can have a negative impact on their personal credit score.

Venture Debt vs. Traditional Bank Loans

While venture debt can be a useful financing option for early-stage companies, it is important to understand how it differs from traditional bank loans. One key difference is that venture debt lenders are typically more focused on the company’s growth potential and future cash flows, while traditional bank lenders are more focused on the company’s current assets and creditworthiness.

Another difference is that venture debt lenders are often more flexible than traditional bank lenders when it comes to loan terms and repayment schedules. This can be particularly important for early-stage companies that may not have the cash flow to support regular loan payments.

Conclusion

In conclusion, venture debt can be a useful financing option for early-stage companies that want to fund their growth without diluting their ownership. While personal guarantees are often required in venture debt financing, they can provide some benefits in terms of improving loan terms and demonstrating commitment to lenders. However, they can also be a significant risk for the guarantor and should be carefully considered before agreeing to them.

Frequently Asked Questions

Here are some common questions people have about venture debt.

What is venture debt?

Venture debt is a form of financing that is typically used by startups and other high-growth companies. It is a loan that is secured by the company’s assets and is usually provided by a specialized lender. Unlike traditional bank loans, venture debt is often structured as a series of smaller loans that are issued over time.

Venture debt can be an attractive source of financing for companies that are not yet profitable or do not have significant assets to offer as collateral. It can also be a useful tool for companies that want to extend their cash runway without diluting their ownership stake.

What are the benefits of venture debt?

One of the main benefits of venture debt is that it can provide a source of financing for startups and other high-growth companies that may not be able to obtain traditional bank loans. Venture debt lenders typically have a deep understanding of the needs of these types of companies and are willing to take on more risk than traditional lenders.

Another benefit of venture debt is that it can be less dilutive than equity financing. By taking on debt instead of selling equity, companies can maintain a larger ownership stake and potentially capture more of the value they create over time.

What are the typical terms of a venture debt loan?

The terms of a venture debt loan can vary depending on the lender and the specific needs of the borrower. However, some common terms include a fixed interest rate, a maturity date, and a requirement for the borrower to meet certain financial covenants or milestones.

In addition, many venture debt loans are structured with warrants or other equity kickers. These give the lender the right to purchase equity in the company at a discounted price in the future. This allows the lender to capture some of the potential upside of the company’s growth.

What are personal guarantees?

Personal guarantees are a common feature of many types of loans, including venture debt. They are a form of collateral that is provided by the borrower, usually in the form of a personal guarantee from one or more of the company’s founders or executives.

If the company is unable to repay the loan, the lender can pursue the personal assets of the guarantor to collect the debt. Personal guarantees can be a significant risk for founders and executives, as they can put their personal assets, such as their home or savings, at risk.

Does venture debt require personal guarantees?

Many venture debt lenders do require personal guarantees as a condition of the loan. However, this is not always the case. Some lenders may be willing to provide venture debt without requiring personal guarantees, especially if the company has strong financials or other assets that can be used as collateral.

It is important for borrowers to carefully review the terms of any venture debt loan and understand their personal liability before signing on the dotted line.

Personal Guarantees: How Bad Do You Want That Loan?

In conclusion, venture debt is a viable financing option for startups and growing businesses. While it may require personal guarantees, this is not always the case. Venture debt lenders consider various factors before requiring personal guarantees, such as the company’s creditworthiness, revenue, and growth potential.

Moreover, personal guarantees may not be as daunting as they seem. They can be negotiated and limited to a certain amount or time frame, providing a level of protection for the borrower. Personal guarantees also demonstrate a level of commitment and confidence from the borrower, which can strengthen the lender’s trust and willingness to provide financing.

Ultimately, venture debt can be a strategic tool for startups and growing businesses to fund their growth, and personal guarantees should not necessarily deter companies from considering this financing option. It is always important to consult with a financial advisor or attorney and carefully review the terms and conditions before making any decisions.