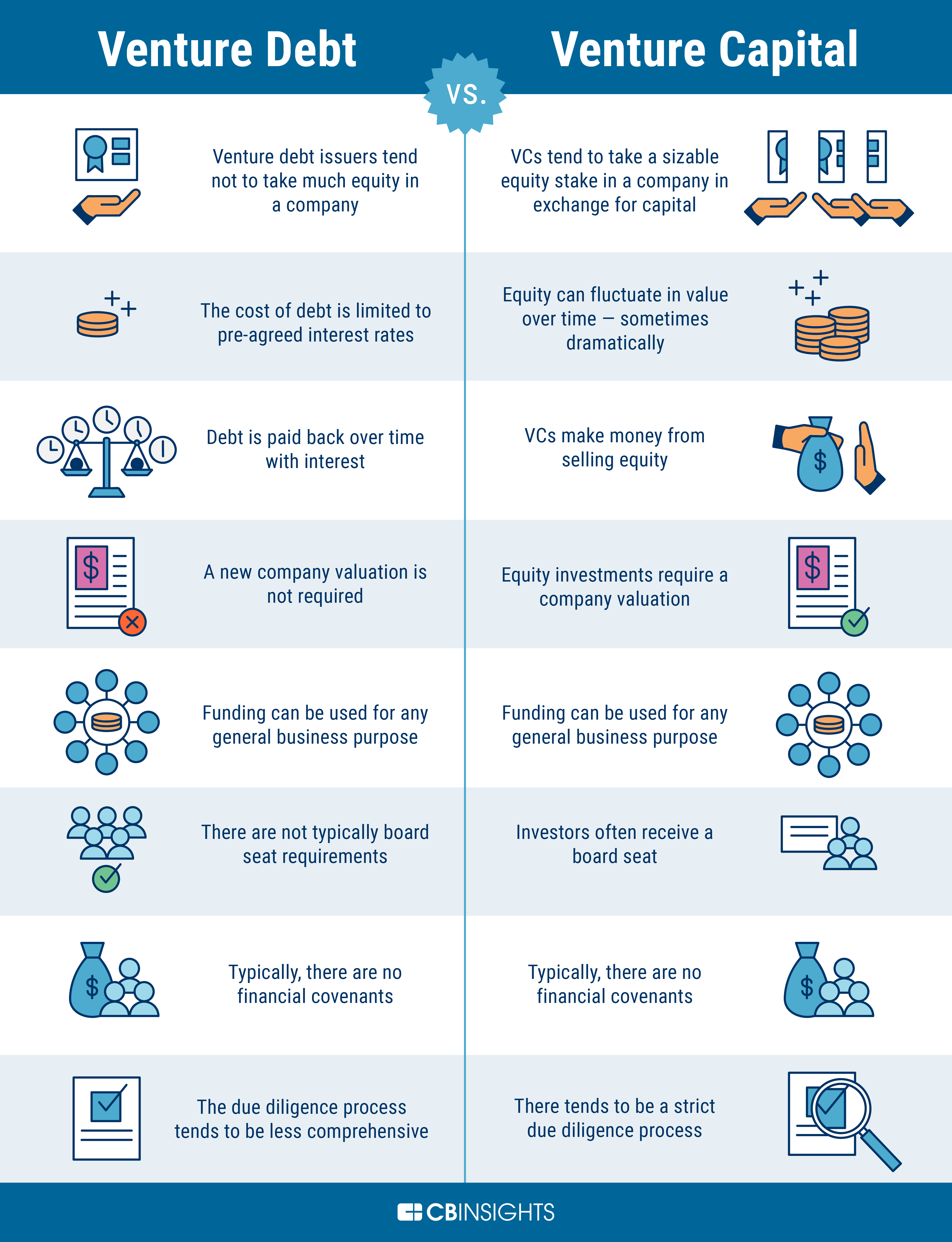

Venture debt lenders play a crucial role in providing financing to startups and emerging businesses. However, it is important for entrepreneurs to understand the terms and conditions of such loans. One of the key factors to consider is whether venture debt lenders have covenants in place, which could impact the borrower’s ability to operate and grow their business.

In this article, we will explore the topic of covenants in venture debt lending. We will discuss what covenants are, why they are used, and the potential implications for borrowers. Whether you are an entrepreneur seeking venture debt financing or simply curious about the world of startup finance, this article will provide valuable insights into the world of venture debt lending.

Did Not Venture Debt Lenders Have Covenants?

When it comes to business financing, debt is often the go-to option for many entrepreneurs. However, not all debt is created equal, and venture debt is a popular choice for startups and other high-growth companies. But with venture debt, come covenants that might limit a company’s ability to operate as they see fit.

What are Venture Debt Covenants?

Venture debt covenants are restrictions that lenders place on borrowers to ensure that they meet specific financial and operational requirements. These covenants are designed to protect the lender’s investment and minimize the risk of default. Covenants can vary depending on the lender, but they typically include financial ratios, revenue targets, and other performance metrics.

The most common types of venture debt covenants include financial maintenance covenants, which require the borrower to maintain specific financial ratios, such as debt-to-equity or interest coverage ratios. Information covenants require the borrower to provide regular financial and operational reports to the lender. Negative covenants limit the borrower’s ability to take certain actions, such as selling assets or acquiring other companies.

Do Non-Venture Debt Lenders Have Covenants?

Yes, non-venture debt lenders also have covenants. However, the covenants may differ from those found in venture debt agreements. For example, traditional bank loans may have fewer or less restrictive covenants than venture debt agreements. This is because traditional bank loans are typically secured by collateral, such as real estate or equipment, while venture debt loans are unsecured.

The Benefits of Venture Debt Covenants

While venture debt covenants can limit a borrower’s freedom of action, they can also provide several benefits. For one, they can help borrower companies stay on track financially by providing regular benchmarks for performance. They can also help companies avoid running afoul of their lender’s expectations, which can result in financial penalties or even default.

Venture debt covenants can also provide some protection to the lender by ensuring that the borrower remains financially healthy. This, in turn, can help the lender’s investment grow as the borrower continues to succeed.

Venture Debt Covenants vs. Equity Financing

Venture debt covenants are not the only option for startups and other high-growth companies. Equity financing, such as venture capital or angel investing, can also provide the necessary funding without the restrictions of debt covenants. However, equity financing typically requires giving up a portion of the company’s ownership or control, which may not be desirable for all entrepreneurs.

Venture debt covenants, on the other hand, provide a way to access capital while retaining control of the company. While the covenants may limit the company’s actions, they can also provide a level of discipline and structure that can be beneficial for growth.

Conclusion

In conclusion, venture debt lenders do have covenants, which are designed to protect the lender’s investment and ensure the borrower’s financial health. While these covenants may limit a company’s freedom of action, they can also provide benefits such as regular benchmarks for performance and protection for the lender. Overall, venture debt covenants can be a useful tool for startups and other high-growth companies looking to access capital while retaining control of their business.

Frequently Asked Questions

What are debt covenants?

Debt covenants are agreements made between a borrower and lender that outline financial and operational requirements the borrower must meet to avoid defaulting on the loan. These requirements are put in place to mitigate the risk of the borrower defaulting on the loan and ensure the lender gets paid back.

Debt covenants can include restrictions on financial performance, such as maintaining a certain debt-to-equity ratio or minimum cash balance, or operational performance, such as limits on capital expenditures or changing business lines.

Why would venture debt lenders not have covenants?

Venture debt lenders may not require covenants because they are typically lending to early-stage companies that are not yet generating significant revenue or have limited operating history. As a result, traditional financial metrics may not be applicable or meaningful. Additionally, venture debt lenders may be more focused on the company’s growth potential and may be willing to take on more risk without the need for covenants.

However, some venture debt lenders may still require covenants depending on the specific terms of the loan and the risk appetite of the lender.

What are the risks of not having covenants?

The main risk of not having covenants is that the borrower may be able to operate the business in a manner that is not in the best interest of the lender. Without covenants, the lender has limited control over the borrower’s actions and may not be able to take corrective measures if the borrower’s financial or operational performance deteriorates.

Additionally, without covenants, the lender may not have a clear picture of the borrower’s financial health and may not be able to anticipate potential issues that could impact the borrower’s ability to repay the loan.

What are the benefits of not having covenants?

The main benefit of not having covenants is that the borrower has more flexibility in managing the business without the restrictions imposed by the lender. This can be particularly important for early-stage companies that are still developing their business models and may need to pivot or change direction quickly.

Additionally, not having covenants can be more cost-effective for the borrower since there are fewer legal and administrative costs associated with monitoring and reporting financial and operational metrics to the lender.

What alternatives are there to debt covenants?

Alternative financing structures, such as revenue-based financing or royalty financing, may not require traditional debt covenants. These structures typically involve the lender receiving a percentage of the borrower’s revenue or royalties in exchange for funding.

Another alternative is to negotiate more flexible covenants, such as allowing the borrower to exceed certain financial ratios if they achieve a certain level of revenue growth. This can provide the borrower with more flexibility while still providing some protection for the lender.

What Happens When A Business Starts Missing Debt Covenants?

In conclusion, we have discovered that venture debt lenders do indeed have covenants. These covenants are put in place to protect the lender’s investment and ensure that the borrower meets certain financial and operational requirements. While venture debt may seem less restrictive than traditional bank loans, these covenants are still important to consider when taking on this type of financing.

It is important for borrowers to carefully review and understand the covenants in their venture debt agreements. Failing to meet these requirements can result in default and potentially harm the borrower’s relationship with the lender. However, when managed properly, venture debt can be a valuable financing option for startups and growing businesses.

Overall, while venture debt lenders may not have as many covenants as traditional bank lenders, they still have measures in place to protect their investment. Borrowers should carefully consider these covenants and work with their lenders to ensure they are meeting all requirements and maintaining a positive relationship.